How many points can credit repair increase in 60 days?

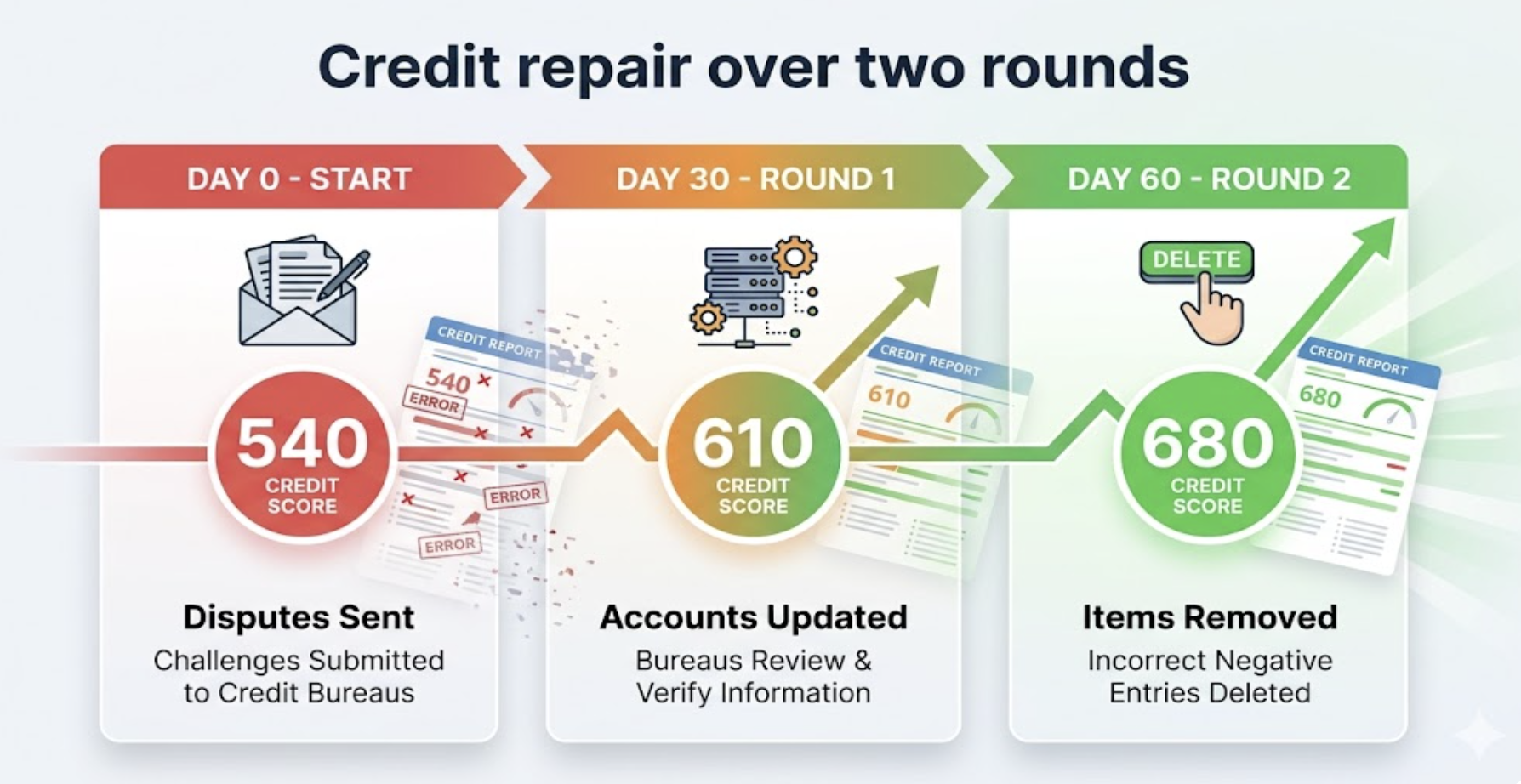

The straight answer will be depending on what is being reported and what gets corrected at that time. Under the Fair Credit Reporting Act, credit bureaus generally have 30 days to investigate disputes. That timeline is what creates “rounds” in credit repair. Each round is one full cycle of disputes, responses, and updates to the report.

After working on credit files for nearly two decades, the pattern is consistent. Most real movement happens between rounds, not overnight. In the first 30 days, some accounts are verified, some are corrected, and some are removed. The second 30 days build on that. If negative accounts come off or balances are updated, the score responds. If nothing changes on the report, the score does not move.

In actual cases, a 60-day increase can range from little to significant. Files with high utilization or reporting errors can see faster gains. Files with multiple charge-offs or recent late payments move slower. The number is not fixed. It is tied to what changes in the report during those two cycles.

Credit Repair Results · How Many Points in 60 Days · Credit Dispute Rounds · What Credit Repair Can and Cannot Do · Realistic Expectations

Updated April 2026 · Written from 20 years of credit repair experience · Sources: FTC Credit Report Accuracy Study, NerdWallet credit dispute guide, CNBC Select credit reporting errors report (2025), CFPB dispute timeline guidelines

People ask me this question more than any other. "How fast can you fix my credit?" The honest answer is: it depends on what is broken. Credit repair is not magic. It is a legal process that works best when there is something fixable on your report. Let me show you exactly what that looks like.

How Many Points Can Credit Repair Increase in 60 Days?

Here is how that plays out by starting situation. I pulled data from the cases we see most often:

| Your Starting Situation | Expected Points in 60 Days | What Drives the Gain |

|---|---|---|

| Errors + high utilization (most common) | 50 to 100+ | Error removal + balance paydown working together |

| Multiple old collection accounts | 40 to 80 | Pay-for-delete or successful disputes on older collections |

| High credit card balances only (no other negatives) | 30 to 70 | Utilization drops fast when balances drop |

| One or two errors, otherwise clean | 20 to 50 | Depends on how much weight the removed item carried |

| Recent accurate late payments (last 12 months) | 0 to 25 | No dispute can remove accurate recent marks. Time is the only fix. |

| Bankruptcy in last 2 years | 0 to 20 | Bankruptcy stays 7 to 10 years. Gains come from rebuilding, not removing. |

The most common mistake I see people make is disputing accurate items. Disputing something that is correctly reported does not remove it. It can actually update the date on the entry, making it look newer. Dispute only what is wrong. Everything else requires time.

What Is a Round in Credit Repair?

Here is how the rounds work in sequence:

Two collections and a charge-off in 60 days is not unusual. It is what happens in Round 1 when those items are old, unverifiable, or contain errors. The FTC study on credit report accuracy found that 4 out of 5 consumers who filed disputes experienced some modification to their credit report. That is not 4 out of 5 getting their score fixed. It is 4 out of 5 getting at least something changed. Those are good odds for first-round disputes. The FTC's full credit report accuracy study also found that approximately 1 in 20 consumers had a maximum score change of more than 25 points from disputes alone, and only 1 in 250 saw a change of more than 100 points from disputes alone. Larger gains require combining disputes with utilization management and pay-for-delete.

According to NerdWallet's credit dispute guide, bureaus must investigate your dispute within 30 days under the Fair Credit Reporting Act, with a 45-day window in some cases. They have five business days after completing the investigation to notify you of the results. That 30-to-45-day cycle is why one round takes about six weeks from start to finish.

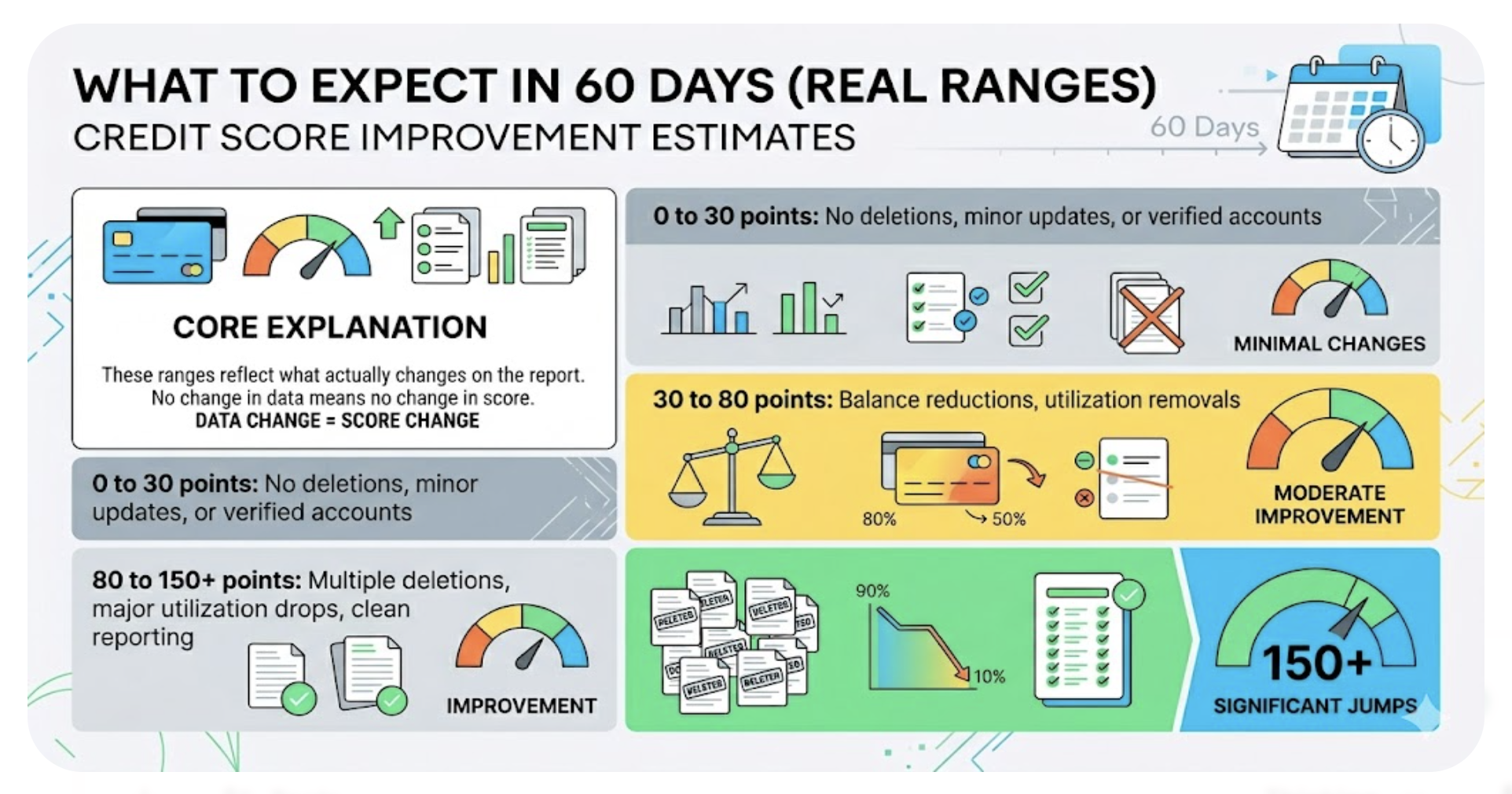

What Does the Data Say About Credit Repair Results?

The chart shows what I tell every new client. The score jumps do not come evenly over time. They come in steps. When a collection gets deleted, the score jumps. Then it holds steady until the next deletion or positive change. This is not like a savings account growing with interest. It is more like stairs. You stay on the same step until something changes, then you go up.

The flat yellow line at the bottom is the hardest truth I deliver. If your only problem is valid recent late payments, 60 days does very little. You are waiting for those marks to age. A 30-day late from six months ago carries less weight than one from last month. At two years old, it barely affects your score. At seven years old, it falls off completely. No dispute letter changes this math.

What Is the Must-Do List During Credit Repair?

- Pay every current bill on time, every month, without exception. One new 30-day late during repair can erase two rounds of progress.

- Pay credit card balances below 10% of each card's limit before the statement closing date, not the due date.

- Pull your three credit reports monthly and track what changes. Check that deleted items stay deleted.

- Request a pay-for-delete agreement in writing before paying any collection account.

- Dispute at the furnisher level (FCRA Section 623) when bureau disputes come back verified.

- File a CFPB complaint on items that bureaus verify but you can prove are wrong. Creditors respond faster to federal complaints.

- Do not apply for new credit during active repair. Each hard inquiry drops your score and signals risk to lenders.

- Do not close old credit card accounts. Closing them raises your utilization ratio and shortens your account age.

- Do not dispute accurate negative items. Disputing correct information can reset the date, making the item look newer.

- Do not pay a collection without a written pay-for-delete agreement. Payment alone changes the status, not the existence of the mark.

- Do not send bulk disputes. Disputing ten items at once triggers a frivolous dispute flag and the bureau can dismiss the entire batch.

- Do not ignore a collection that is within the statute of limitations. Ignoring it risks a lawsuit and a judgment.

The bulk dispute warning is one most people learn the hard way. I have seen clients send 15-item dispute letters and get every single one dismissed as frivolous. The bureaus have the right to do that under the FCRA. The correct approach is to dispute strategically, starting with the clearest and most impactful items, then working through the rest in subsequent rounds. Three to five items per round is the right pace.

If you are surprised by how your score is moving during repair, understanding what causes scores to drop in the first place helps you avoid creating new problems while fixing old ones. Our guide on the most common reasons a credit score drops 50 points overnight covers the specific triggers that can undo credit repair progress while it is happening.

Does Paying On Time Fix Your Credit Score by Itself?

This is one of the most common questions I get. "I've been paying on time for a year. Why isn't my score going up?" The answer is that on-time payments prevent your score from getting worse. They build positive history. But existing negatives continue to count until they are removed or until they age off the report. The negative mark from two years ago and the positive marks from the last 12 months both live on your report simultaneously. The score reflects all of it.

That scenario is the most common one I see. The person is doing everything right now. But the old marks are still there. The question to ask is: can those 2020 collections be disputed, negotiated for pay-for-delete, or are they verified accurate? If they can be disputed because of a reporting error, they may come off before 2027. If they are accurate, paying them does not remove them, but FICO 9 ignores paid collections entirely, so getting them paid to zero changes how newer scoring models treat them.

People sometimes see their score drop even when they are doing everything right. If that has happened to you during the repair process, the breakdown of why your credit score goes down when you pay on time explains the specific mechanics behind this, including how new accounts, credit limit changes, and reporting timing all affect your score independently of your payment behavior.

What Numbers Should You Realistically Expect?

The fastest gains happen in the first 30 to 60 days for clients who have high utilization and at least one removable item. After that, the pace slows because the easy wins are done. Months 3 through 6 focus on stubborn items, pay-for-delete negotiations, and building clean history. Month 6 onward is mostly about time. Negative marks weigh less as they age. On-time history grows longer. The score rises, but more slowly.

A 2024 Consumer Reports study found that nearly half of consumers who reviewed their credit reports found at least one mistake. Roughly a quarter of them found errors that could negatively impact their score. As reported by CNBC Select's analysis of credit reporting errors, the credit reporting agencies received nearly five million complaints to the CFPB in 2025, up from 1.3 million in 2023. That volume reflects growing awareness, not necessarily more errors. More people are checking their reports and finding what has been there all along.

That result, 188 points over 8 months, is at the top of what most people can realistically achieve. It required four removable items, two errors, and disciplined utilization management over the full period. This is not a typical result. The typical result for someone who starts with a 490 to 550 score and has multiple disputable items is 80 to 130 points over six months. Not 188. Not 50. Somewhere in that range, with the pace of gains front-loaded in the first two rounds.

If your score is currently at 400 and you want to understand the full roadmap to recovery, our guide on the path to increasing a 400 credit score covers the unique challenges of rebuilding from the very bottom, including what secured credit options exist, how long each stage of rebuilding takes, and what milestone scores unlock meaningful financial options.

What Should You Not Do During Credit Repair?

The second biggest mistake is paying a collection without a pay-for-delete agreement. I still talk to people every week who paid a collection three years ago, the mark is still on their report, and they cannot understand why. Paying a collection changes the status from unpaid to paid. Under FICO 8, the most common scoring model, a paid collection still counts against you. The entry stays for 7 years from the date of first delinquency. The only way to get rid of it before that is deletion: either through a dispute or a pay-for-delete agreement negotiated before payment.

Find Out What Is Fixable on Your Report in the First 60 Days

A free 3-bureau audit pulls your Experian, TransUnion, and Equifax reports and identifies every item that is disputable, every collection that qualifies for pay-for-delete, and what your score could look like in 60 days based on what we find.

Get My Free Credit Audit → Secure · 2 minutes · No credit card requiredFrequently Asked Questions

How many points can credit repair increase your score in 60 days?

The typical range is 40 to 100 points in 60 days for clients with removable errors or collection accounts and high credit card balances. Some clients see less than 20 points if their problems are accurate recent late payments that cannot be disputed. Some clients see more than 100 points if they have multiple removable items and high utilization that drops significantly in the first billing cycle. There is no single answer because the result depends on what is on your report.

What is a round in credit repair?

A round is one complete cycle of the dispute process. You send letters to the credit bureaus, wait 30 to 45 days for them to investigate, review the results, and plan the next move. One round takes 35 to 50 days. Most people need 2 to 6 rounds to complete credit repair. A single round covers roughly 60 days when you include the investigation period and time to review results and send the next set of letters.

Is credit repair worth it?

Credit repair is worth it when your report contains errors, outdated items, or unverifiable accounts that can be disputed and removed. The FTC found that 1 in 5 consumers has an error on at least one credit report that was corrected after being disputed. About 20% of those who had errors corrected moved into a better credit risk category. If your report is accurate with no removable items, credit repair produces less in the short term, but the dispute process and credit building strategies still matter for long-term score health.

What should you not do during credit repair?

Do not apply for new credit, close old accounts, dispute accurate items, pay collections without a written pay-for-delete agreement, or miss any payment on current accounts. Each of these either directly damages your score or removes the leverage that makes the repair process work. The two most common self-sabotaging moves are applying for credit too early, which adds a hard inquiry and lowers account age, and paying collections without securing deletion first.

How long does one round of credit repair take?

One round takes 30 to 45 days for the bureau investigation, plus five additional business days for them to notify you of the results. Plan for 35 to 50 days per round total. Under the Fair Credit Reporting Act, bureaus must investigate disputes within 30 days, or 45 days if you submit additional information during the investigation or if you filed after receiving your free annual credit report.

How many points does credit repair add per month?

Credit repair does not add points evenly month by month. Progress comes in jumps when items are removed. A month with a deletion might add 30 to 100 points in one reporting cycle. A month with no deletions might add zero points, even if you are doing everything right. The average score improvement for consumers who had errors corrected was around 25 points, according to FTC research, but that is an average across many cases including those where only minor items were removed.

-

What Credit Score Is Needed for a Zero Down Mortgage? If credit repair is your path to buying a home with no down payment, this covers the exact score thresholds for VA and USDA loans, what the average approved borrower actually looks like, and which lenders accept lower scores.

-

How to Go From 500 to 700 Credit Score Fast The step-by-step plan for the full 500-to-700 journey: what moves the score fastest, the AZEO utilization strategy used by top FICO scorers, and realistic timelines for each phase of the rebuild.

-

Is 686 a Good Credit Score? After credit repair gets you to the 680 range, this breaks down what you can actually get approved for at that score, what rates you pay versus someone at 720, and the next steps to the tier that unlocks best-available rates.

60 Days Credit Repair

In 60 days, credit repair can produce movement, but only if the report changes. Most people see progress across two rounds, not from a single action. Early gains often come from utilization changes or corrected balances. Larger increases come when negative accounts are removed or stop reporting.

A realistic expectation is not a fixed number. It is a range based on what gets updated. Some files move quickly because the issues are correctable. Others take longer because the accounts are accurate and still within reporting limits.

Credit repair is not about sending disputes and waiting. It is about controlling what gets reported each cycle. When that changes, the score follows.