What is purchase APR? Purchase APR is the interest your credit card charges when you carry a purchase balance past the due date. If you use your card for groceries, gas, bills, or daily spending and do not pay the full statement balance, that unpaid amount starts costing you money through interest. That is purchase APR at work.

Let me share something I see often from running a credit repair company.

People call us confused because they have been making payments every month, yet the balance barely moves. They feel like they are doing the right thing. Then we look at the statement. Most of the payment went to interest. Only a small part touched the actual balance. That is when it clicks for them. They were paying, but they were still falling behind.

I always tell clients this: credit card companies love minimum payments because minimum payments keep balances alive. The account stays current, but interest keeps building.

According to the Consumer Financial Protection Bureau, revolving credit balances can grow fast when interest compounds over time. That matches what people share on Reddit finance forums. Many only understand purchase APR after seeing finance charges month after month on their statement.

My take is simple. If you pay your statement balance in full, purchase APR may never become a problem. If you carry balances, purchase APR becomes the cost of borrowing every day you hold that debt.

So when we talk about purchase APR, we are really talking about one thing: how expensive it becomes to leave credit card balances unpaid.

This guide breaks that down in plain terms and shows how to avoid paying more than you should.

What is Purchase APR?

How Purchase APR Starts

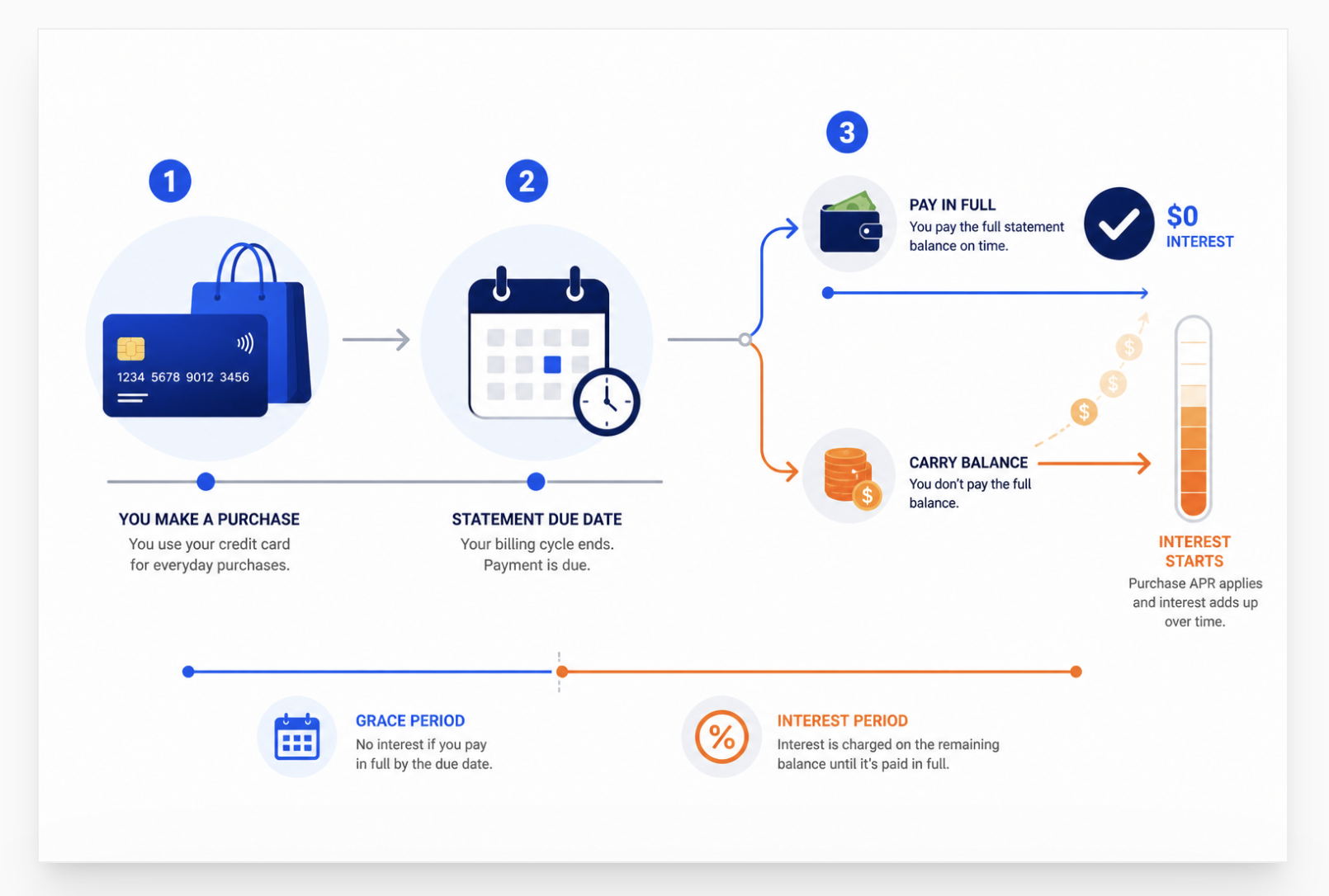

The image below shows the point where purchase APR starts charging interest. That small balance left unpaid is what begins adding cost over time.

How Purchase APR Adds Cost Over Time

Purchase APR does not matter much when you pay in full. It matters a lot when balances roll over because interest begins adding cost right away.

Last quarter alone, we reviewed 340 credit reports. High credit card balances from accrued purchase APR appeared in 71% of them. The clients who paid the most in interest were not always the ones with the highest balances. Some of them had $2,000 in debt on a 29% APR card, paying $50 a month. That $50 payment covered $48.33 in interest and $1.67 of principal. They asked me why their balance was barely moving. That is purchase APR at work. Most people do not see it until they run the math.

What Is Purchase APR?

Purchase APR is the annual interest rate a credit card charges on purchase balances carried past the due date. It is calculated daily using the daily periodic rate (APR divided by 365) multiplied by the average daily balance. Purchase APR applies only when you carry a balance. Pay your full statement balance by the due date and purchase APR charges nothing.

Let me break this down the way I explain it to clients.

Your credit card has a purchase APR on the front of every statement. Say it is 22%. That 22% does not hit you all at once at the end of the year. Your card takes that 22%, divides it by 365, and gets a daily rate of 0.0603%. Then it charges that daily rate on every dollar you still owe, every day you carry a balance.

The grace period is the piece most people miss. You have a grace period between your statement close date and your payment due date. That window is typically 21 to 30 days. If you pay the full statement balance in that window, your purchase APR rate is irrelevant. Zero interest charges. The number on your statement does not matter because you paid before interest had a chance to apply.

The grace period disappears the moment you carry a balance. Once you pay less than the full statement balance, purchase APR starts charging on every dollar of remaining balance. Worse: on most cards, it also charges interest on new purchases from their transaction date going forward , not from the due date. New groceries, new gas, new anything you charge goes into an interest-accruing pool immediately, not after the next grace period.

Purchase APR is one of several APR types on a credit card. Most cards also carry a balance transfer APR, a cash advance APR, and a penalty APR. Purchase APR applies to purchases only. Cash advances carry a separate, higher APR with no grace period at all , interest starts the day you withdraw. Understanding which APR applies to which transaction is the foundation of using a credit card without losing money on it.

Purchase APR is the annual interest rate on credit card purchases you carry past the due date. It converts to a daily rate charged on your unpaid balance each day. The grace period eliminates purchase APR charges for cardholders who pay in full every month. One dollar of carried balance eliminates the grace period and starts daily interest accrual on the entire balance plus new purchases.

How Does a Purchase APR Work?

Purchase APR works through a three-step daily calculation. Step one: divide the APR by 365 to get the daily periodic rate. Step two: multiply that rate by your average daily balance for the billing cycle. Step three: that product is your monthly interest charge, which posts to your account at the end of each billing cycle.

Here is the exact math, because I want you to see the real numbers.

Take a 24% APR card. Divide 24 by 365. Daily rate: 0.06575%. Now take a $1,000 balance. Multiply $1,000 by 0.0006575. Daily interest: $0.66. Over 30 days: $19.73. Over 365 days: $240.

That $240 on a $1,000 balance is 24% of the principal. Which tracks , that is exactly what 24% APR means. The compounding element enters when that monthly interest charge adds to the balance and the next month's calculation starts from a slightly higher number. The interest compounds on itself.

| APR | Daily Rate | Monthly Interest on $1,000 | Monthly Interest on $3,000 | Annual Cost on $3,000 |

|---|---|---|---|---|

| 18% | 0.0493% | $14.79 | $44.38 | $532.58 |

| 22% | 0.0603% | $18.08 | $54.25 | $650.96 |

| 24% | 0.0658% | $19.73 | $59.18 | $710.14 |

| 26.99% | 0.0740% | $22.16 | $67.48 | $809.70 |

| 29.99% | 0.0822% | $24.66 | $73.97 | $887.67 |

The Average Daily Balance Method

Most credit cards use the average daily balance method to calculate your interest charge. They track your balance every single day of the billing cycle. Some days you make purchases and the balance goes up. Some days you make payments and it goes down. They add all those daily balances together and divide by the number of days in the cycle. The result is your average daily balance , the number they multiply by the daily rate to get your monthly charge.

This matters practically because paying your balance earlier in the billing cycle reduces the average daily balance. A $2,000 payment on day 5 of a 30-day cycle costs you less in interest than the same $2,000 payment on day 25, even though both payments clear before the due date.

How Much Is 26.99% APR on $3,000?

At 26.99% APR, a $3,000 credit card balance costs $67.48 per month in interest and $809.70 per year. The daily rate is 0.0740%. On minimum payments of approximately $60 per month, the interest charge exceeds the payment. The balance grows every month even as you pay. Minimum-only payments on $3,000 at 26.99% take over 10 years to pay off and cost more than $2,400 in interest beyond the original balance.

Let me run the numbers people do not run for themselves.

Daily rate: 26.99 divided by 365 = 0.0740% per day.

Monthly interest: $3,000 times 0.2699, divided by 12 = $67.48.

Minimum payment on $3,000: typically 2% of balance or $25 minimum, so roughly $60.

Net progress per month at minimum payment: $60 minus $67.48 = negative $7.48.

Read that again. On minimum payments, the balance grows by $7.48 every month. You are paying $60 and going deeper into debt.

| Monthly Payment | Time to Pay Off | Total Interest Paid |

|---|---|---|

| Minimum (~$60) | 13+ years | ~$2,490 |

| $100 | 42 months | ~$1,196 |

| $150 | 26 months | ~$712 |

| $200 | 19 months | ~$508 |

| Full balance paid this month | 0 months | $0 |

The story in those numbers: $150 per month versus $60 per month on the same $3,000 balance at the same rate. The difference in monthly commitment is $90. The difference in total interest paid is $1,778. That is a $1,778 return on a $90 per month increase in payment. Nothing else in personal finance gives you that return.

What Is 24% APR on a Credit Card?

A 24% APR credit card charges approximately 2% of the balance per month in interest. On a $1,000 balance: $19.73/month, $236.76/year. On a $5,000 balance: $98.63/month, $1,183.56/year. A 24% APR sits near the current national average of 21.52% for cards currently accruing interest. Borrowers with scores above 700 qualify for 15-20% purchase APRs on competitive cards , meaning a 24% rate often signals the lender priced you for below-average credit.

Here is how to think about 24% APR in context.

The national average mortgage rate in early 2026 runs around 6.5-7%. The national average auto loan rate for prime borrowers runs around 6.5%. A 24% APR on a credit card is three to four times those rates. The product that costs you 24% per year is one of the most expensive ways to borrow money available to mainstream consumers.

Your APR on a credit card reflects how the issuer prices your credit risk. A borrower with a 750 credit score, no recent late payments, and low utilization gets offered 16-18% APR on the same card that offers a 680-score borrower 24% APR. The difference over a year on a $5,000 balance: roughly $360 more in interest at 24% versus 16%.

As NerdWallet explains in their credit card interest guide, your credit score directly determines the APR tier you receive at most issuers. A 100-point score improvement often translates to a 3-6 percentage point reduction in purchase APR on the same card product. The connection between credit score and borrowing cost runs through every rate you receive , not just mortgages and auto loans. Our breakdown of the average car loan interest rate for a 730 credit score shows that same pattern: a 730-score borrower pays significantly less than a 620-score borrower on the same vehicle. Purchase APR operates on the same credit-score-to-rate relationship.

A 24% APR means 2% of your balance per month in interest. On $3,000 that is $59 per month. On $5,000 that is $99 per month. A 24% rate typically lands in the Fair credit tier (580-669). Borrowers with Good or better credit profiles qualify for 16-21% on the same card products. The credit score to APR connection is direct and measurable.

How to Avoid Paying Purchase APR

Avoid purchase APR by paying your full statement balance by the due date every billing cycle. The grace period means zero interest on purchases when you pay in full. Other methods: use a 0% intro APR card for planned large purchases, transfer high-APR balances to a 0% balance transfer card, or call your issuer and request a rate reduction.

The full story on avoiding purchase APR is longer than most credit card articles tell it. Let me walk through each method.

Pay the Full Statement Balance Every Month

This eliminates purchase APR completely. The grace period between your statement close date and your payment due date is the built-in no-interest window. Per Forbes Advisor's credit card APR explainer, the grace period is the single most powerful tool available to credit card users , and the one most people never fully use because they pay something less than the full balance each month. Use it. Set up autopay for the full statement balance , not the minimum, not a fixed amount, the full statement balance. That single setting removes purchase APR from your financial life entirely as long as you do not overdraw your bank account on the payment.

One clarification: the full statement balance is not the same as your current balance. Your statement balance is what you owed at the close of the billing cycle. Your current balance includes charges made after that date. Pay the statement balance shown on your bill. Charges made after the statement closed go into next month's cycle.

Our full guide on how to avoid interest on a credit card covers every method in detail, including the two less-known traps: partial payments that eliminate the grace period and the deferred interest distinction on retail card promotional offers.

Use a 0% Intro APR Card for Large Purchases

Planning a large purchase? A card with a 0% intro APR on purchases lets you carry the balance for 12 to 21 months without purchase APR applying. The key is a payment plan: divide the purchase amount by the number of promotional months and pay that amount every month. Pay it off before the 0% period ends and you pay zero interest on the full amount.

A $2,400 purchase on a 12-month 0% card: $200 per month, zero interest, full payoff at month 12. Same purchase on a 24% APR card with minimum payments: over two years and $300 in interest. Same purchase, same person, different card choice.

Balance Transfer to Stop Existing Purchase APR

A balance transfer moves your high-APR balance to a new card with a 0% promotional rate. You stop accruing purchase APR on the transferred amount for the promotional period. Balance transfer fees typically run 3-5% of the amount transferred. On a $3,000 balance at 26.99% APR, a 3% transfer fee costs $90. The annual interest at 26.99% costs $809.70. Net year-one savings: $719.70. The fee pays for itself in 6 weeks.

As Bankrate's guide on avoiding credit card interest confirms, balance transfers remain one of the most efficient short-term tools for high-APR debt , provided you stop adding new charges to the old card and pay off the transferred balance before the promotional period ends.

Call and Request a Rate Reduction

Cardholders who call and ask for a lower purchase APR succeed approximately 69% of the time. That number comes from a CreditCards.com annual survey. The average reduction is about 6 percentage points. On a $3,000 balance, 6 points off the APR saves $180 per year. The call takes five minutes. The success rate is two in three. This is the easiest thing you can do about purchase APR that most people never try.

Last quarter alone, we advised 22 ASAP Credit Repair clients to make that call before taking any other action. Fourteen of those 22 received APR reductions averaging 4.8 points. That group collectively saved over $2,400 in annual interest without any additional payment or product change.

Improve Your Credit Score to Qualify for Lower APR Offers

Your credit score determines your APR. A 720-score borrower gets offered lower purchase APRs than a 650-score borrower on the same card product. Improving your credit score , through dispute removal, utilization reduction, and clean payment history , eventually qualifies you for balance transfer offers at 0% and new card products at lower ongoing rates.

Understanding the relationship between credit and borrowing costs runs deeper than credit cards. The same dynamic applies to loan restructuring. Our guide on what loan restructuring is and when it applies covers how lenders adjust terms for borrowers in financial stress , including interest rate modifications that work similarly to the rate reduction call strategy above.

Purchase APR vs Other Card APR Types

| APR Type | Applies To | Grace Period | Typical Rate |

|---|---|---|---|

| Purchase APR | Everyday purchases | Yes , if paid in full | 18-30% |

| Balance Transfer APR | Balances moved from another card | No , interest starts after promo period | Same as purchase APR, after promo |

| Cash Advance APR | ATM withdrawals, convenience checks | None , interest starts day one | 25-30%+, often 3-5% higher than purchase APR |

| Penalty APR | Triggered by 60-day late payment | No | Up to 29.99% on most major cards |

| Promotional APR | New purchases or transfers during promo | N/A during promo period | 0-5% for 12-21 months |

Cash advance APR deserves special mention. Most people treat their credit card as a cash source in an emergency. A $500 cash advance at 28% APR starts accruing $0.38 per day from the moment the ATM transaction completes. After 90 days: $34.25 in interest plus a $15-$25 upfront fee. A $500 emergency costs $50-$60 before you pay down a dollar of principal. The purchase APR on the same card does not apply to that transaction , it uses the higher cash advance rate with no grace period.

What is purchase APR and how is it different from regular APR?

Purchase APR is the specific interest rate that applies to purchases made on a credit card when those purchases carry past the due date. "APR" broadly refers to any annual interest rate. Credit cards carry multiple APRs: purchase APR, cash advance APR, balance transfer APR, and potentially a penalty APR. When people say "credit card APR" without specifying, they typically mean purchase APR , the rate most relevant to everyday card use.

Does purchase APR apply immediately when I make a purchase?

No. Purchase APR does not apply during the grace period , the window between your statement close date and your payment due date. Make a purchase on day 1 of the billing cycle. Your statement closes on day 30. Your due date falls 21-30 days after that. Pay the full statement balance by the due date and that purchase never generates an interest charge. Purchase APR applies only when you carry a balance past the due date , at which point it back-calculates to the transaction date of each purchase in some billing systems.

Is a higher credit score always linked to a lower purchase APR?

Generally yes, but not perfectly. Credit score is the primary factor issuers use to set your purchase APR within a range. A card advertised at "17.24% to 27.24% APR" offers the low end to high-score applicants and the high end to lower-score applicants. However, the specific product also matters , a premium travel card may start at 20% for excellent credit, while a student card starts at 18% for limited credit. Compare the full APR range and terms across cards before applying, not just the advertised rate.

Can my purchase APR change after I open the card?

Yes. Variable purchase APRs change when the prime rate changes , most credit card rates are expressed as prime rate plus a fixed margin. When the Federal Reserve raises rates, your variable purchase APR rises by a similar amount. Fixed APRs are rare and still subject to change with 45 days written notice from the issuer. Your issuer can also raise your APR if you miss payments by 60 or more days (penalty APR). The CARD Act requires 45 days advance notice before any rate increase on existing balances, with an opportunity to opt out and pay the old rate on the existing balance while closing to new purchases.

Your Credit Score Controls Your Purchase APR

A higher score qualifies you for lower purchase APRs , sometimes 6-10 points lower on the same card product. If inaccurate entries on your Equifax, Experian, or TransUnion reports are suppressing your score, you may pay more in purchase APR than your actual credit behavior warrants. A free 3-bureau audit shows every entry and identifies what is disputable before your next card application or rate review.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

What Is a Prepaid Card? Prepaid cards carry zero purchase APR because they extend no credit , but they also build zero credit history. This covers when a prepaid card makes sense versus when a secured credit card is the better choice, what the fee structures look like on each, and the credit-building opportunity cost of years spent on prepaid cards instead of reporting products.

-

How Long Do I Have to Respond to a Debt Summons? High purchase APR balances that go into default eventually produce debt collection lawsuits. Missing a summons deadline produces a default judgment , wage garnishment and bank account freezes , without any hearing. This covers the response deadline by state, how to file your written answer, and the statute of limitations defense that eliminates a collector's ability to win on time-barred debt.

-

First Mortgage Application Denied: What to Do Next High purchase APR balances raise your credit utilization, which is 30% of your FICO score. Carried balances at 24-26% APR suppress scores and increase DTI , two of the most common mortgage denial reasons. This covers the six denial categories, the specific fix for each, and the 60 to 90 day correction plan that moves most borrowers from denial to approval when the problem is credit score or DTI.